By Kostya Etus, CFA®, Chief Investment Officer, Dynamic Investment Management

Supportive Trends Fend Off Spooky Season

The market continues its strong run this year with the S&P 500 up over 24% through the end of last week (10/18/24). This is great to see given September and October are typically a weaker time for the markets.1 But despite some uncertainties discusses in the last market update, including a tight Presidential election, the S&P 500 has maintained six straight weeks of gains.2 What is more exciting is that we are on track for a second consecutive years of bull market returns (over 20%), which has only occurred five times over the last 75 years.3

As we head into the holiday months of November and December, which tend to be seasonally strong for the markets, there are a few things to be thankful for which may help alleviate investor scaries:

- Friendly Federal Reserve (Fed): A favorable outlook from the Fed for a lower interest rate policy going forward is supporting for most asset classes, as discussed in the next section.

- Tasty Corporate Earnings: According to Factset, while only 14% of S&P 500 companies have reported earnings, about four out of five have reported a positive earnings surprise.4

- Generous Economic Growth: Strong jobs growth, combined with lower unemployment and sustained lower levels of inflation point to stronger economic growth ahead.

I realize I may have jinxed the markets with this update, as uncertainties still remain, but the treats that the Fed, corporations, and the economy are handing out will be hard to beat.

Backdrop for More Treats to Come

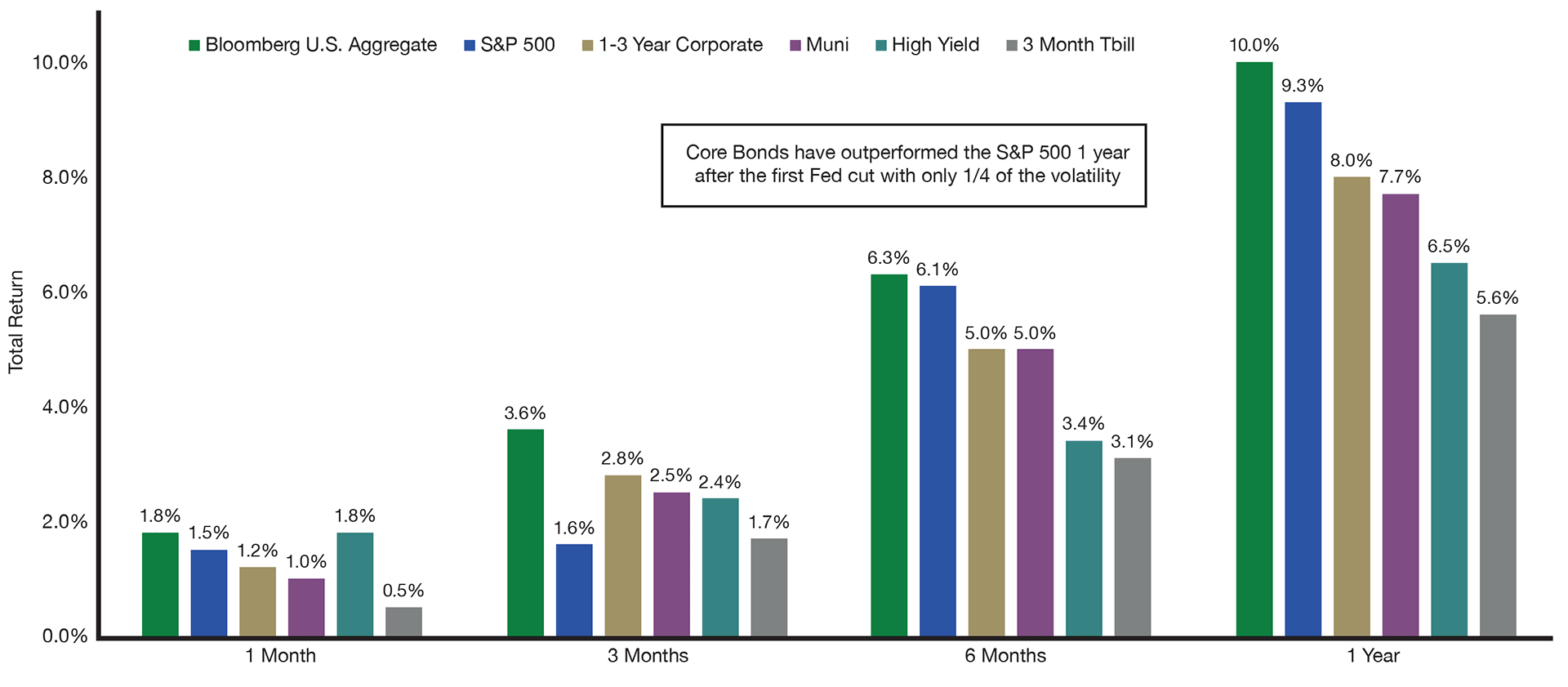

Now that we have had our first interest rate cut from the Fed, as well as a reinforcement of a lower interest rate policy for the foreseeable future, what can we expect from the markets? More importantly what does it mean for various asset classes which investors may be exposed to? As always, let’s take a look at what history can teach us by evaluating the performance of broad asset classes after the initial rate cut over the last seven rate-cutting cycles:

- Most Asset Classes Are Positive: Looking at stocks and a variety of bonds, we find that historically all of the asset classes are up after the first rate cut by the Fed over various time periods.5 More importantly, the longer the time horizon, the stronger the returns, reinforcing the need to stay invested for the long-term.

- Bonds Beat Stocks: Another pleasant surprise is that broad based bonds (green bar) consistently beat stocks (blue bar) over all time periods.6 Given that bond prices increase as interest rates drop, this makes some intuitive sense. This reinforces the idea that the 60/40 is not dead and the importance of staying balanced and diversified with both stocks and bonds within portfolios.

- Anything is Better than Cash: Perhaps the most important takeaway from the chart is that all of the asset classes presented beat cash (grey bar).7 As interest rates drop, it reduces the yield received on short-term cash investments, which have limited ability to appreciate in price. Thus, a falling interest rate environment may be a great opportunity to get off the sidelines and get back into investing with diversified, balanced portfolios for the long-term.

Stay diversified, my friends.

Asset Class Performance Following the First Federal Reserve Interest Rate Cut

(Average of the Last 7 Cutting Cycles)

Sources: Bloomberg Index Services Limited. Past performance is not a reliable indicator or guarantee of future results. Data represents the performance of the Bloomberg U.S. Aggregate, S&P 500, ICE BofA 1-3 Year Corporate Index, Bloomberg Muni Index, Bloomberg U.S. Corporate High Yield Index, and the ICE BofA U.S. Treasury Bill 3 Month Index over the 1-month, 3-month, 6-month, and 1-year, periods following the first Federal Funds rate cut in the previous 7 cycles by the US Federal Reserve. The start date of the 7 periods are 10/2/84, 10/19/87, 6/5/89, 7/6/95, 1/3/01, 9/18/07, and 7/31/19.

As always, we recommend staying balanced, diversified, and invested. Despite short-term market pullbacks, it’s more important than ever to focus on the long-term, improving the chances for investors to reach their goals.

Sources:

- “Here’s Why September and October are Historically Weak for Stocks,” CNBC, Sept. 11, 2024.

- “U.S. Stocks Post Sixth Straight Weeks of Gains, Gold Hits All-Time High,” Reuters, Oct. 18. 2024.

- “The Current Bull Market Just Turned 2. History Has Good News for Investors Just Joining the Party,” The Motley Fool, Oct. 18, 2024.

- “Earnings Insight,” FactSet, Oct. 18, 2024.

- “How Have Key Asset Classes Performed After the Start of Prior Fed Rate Cut Cycles?,” Plante Moran, Sept. 5, 2024.

- “How Could Fed Rate Cuts Affect Asset Returns?,” Allianz Global Investors, April 4, 2024.

- “How Could Fed Rate Cuts Affect Asset Returns?,” Allianz Global Investors, April 4, 2024.